Last month I wrote about the three previous, what I called, “panic markets” in order to give perspective and remind ourselves that these severe drops do end, and eventually lead higher to new all-time highs.

In his 2016 annual letter to shareholders, Warren Buffett made several statements that I believe are critically important for investors to remember during this current tumultuous market period. One of the best, which I believe so aptly describes the current times, is:

“Every decade or so, dark clouds will fill the economic skies, and they will briefly rain gold. When downpours of that sort occur, it's imperative that we rush outdoors carrying washtubs, not teaspoons. And that we will do."

We have always liked to frame these occasional sharply lower markets as times when there is a “Big Sale” going on in the stock market. Instead of “washtubs”, we use the analogy of “backing up the truck” to fill it with marked-down items (stocks). If we can remember that falling prices create value while rising prices extinguish value, then we can see these infrequent periods for the opportunities (“gold rain”) that they truly are.

I want to be clear that I am not calling March 23, 2020 as “the bottom”. Neither I, nor anybody else, knows for sure. However, what I do know is that most investments have seriously lagged the two big winners from the 2009-2020 bull market. The big winners were large-cap U.S. stocks as represented by the S&P 500 as well as government debt, particularly U.S. treasuries. Some of the laggards include smaller U.S. company (small-cap) stocks, international stocks, value stocks, and natural resources stocks. Furthermore, during the recent tumult as the world sought safe havens, the outperformance of the S&P 500 and treasuries became even more extreme. At some point, however, maybe whenever the next bull market starts, we would expect some major catching up by the laggards.

I thought I’d highlight a few of these big valuation divergences. This commentary is quite a bit longer than usual as I’ve included some charts for further illustration.

The first chart looks at the relative valuation between the S&P 500 and the 10-year U.S. treasury. The message here is probably how expensive U.S. treasuries are and not how undervalued the S&P 500 is. This Bloomberg chart shows stocks to be the cheapest they have been compared to bonds in nearly 40 years (since 1983). This tells me, “Don’t back up the truck for treasuries”. Yes, they have been a good hedge during the panicky sell off. However, with 10-year notes yielding only 0.75% as I write this, there just is not return to be had. In fact, holding the notes to maturity and paying taxes on income annually would likely generate a loss after inflation.

There are many different definitions for determining what is a “growth” stock and what is a “value” stock. Growth stocks tend to have steadier, increasing earnings and are rewarded with higher valuations, sometimes quantified by their price-earnings ratios. Often, value stocks have more volatile earnings streams, pay higher dividends, and receive lower valuations by the market. The key is that sometimes when the difference in valuations gets stretched enough, it is usually time for value stocks to outperform. Currently the spreads are quite stretched:

While we don’t directly target growth and/or value, we usually divide our allocations between cap-weighted index funds and fundamentally-weighted index funds. These tend to be good proxies for growth and value, respectively.

As you can see from the chart below, small capitalization companies have their lowest relative weight versus large companies than they have had since peak of the dot-com era in the late 1990s. You can also see from the practically straight-down trajectory at the end of this chart that this unusually wide discrepancy widened sharply further during this recent sell off.

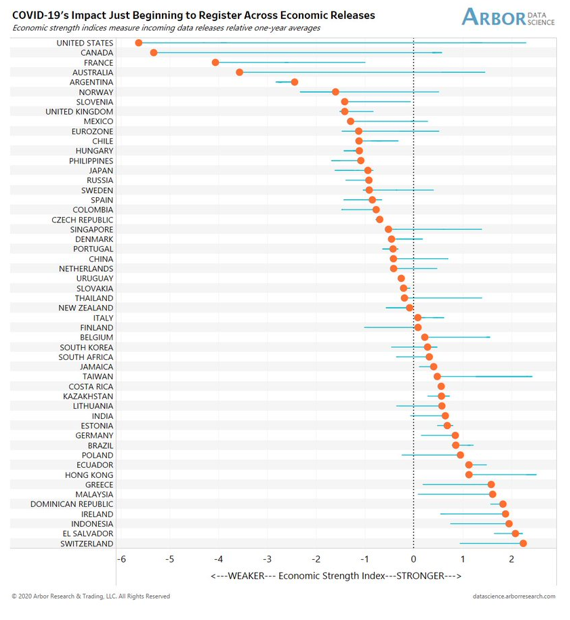

We have written about this many times in the past and the lagging performance of non-U.S. markets has continued. There has been no question that the United States economy has been much stronger than virtually all the non-U.S. economies since the Great Financial Crisis. Yet, at some point that is likely to change and, perhaps more importantly, the difference in economic performance may already be more than priced in for these International stocks.

According to the JP Morgan Guide to the Markets for the 2nd quarter 2020:

Finally, this chart shows that the U.S. is being impacted the most economically by the Covid-19 crisis – perhaps another reason to look overseas.

Finally, after many decades of rising U.S. financial assets – S&P 500 and U.S. treasuries – perhaps it’s time for a reversion to the mean in so-called “real assets” such as commodities. This chart shows that commodities are as radically undervalued as they have been in the last 100 years.

We are living through extraordinary times in so many ways. Certainly, this fastest decline from an all-time market high to a bear market has been stunning. In this commentary, I’ve tried to point out that there are many, many relative valuation extremes as well. The extremes may continue and even become more extreme for a while longer, though at some point they will, at a minimum, mean-revert if not overshoot in the other direction. We will want to be on board when that happens. Remember that diversifying into relatively cheaper asset classes not only smooths the ride but also offers great potential for outsized gains. Keep patient and stay diversified as eventually the extreme relative positions will revert to the mean. Hold onto small stocks, international stocks, value stocks (e.g. fundamental index funds), natural resources (commodity-focused) stocks, while continuing to hold onto the large-cap U.S. stocks that have been the leaders to-date.

Finally, one other quote from that Warren Buffett annual letter:

Moreover, the years ahead will occasionally deliver major market declines -even panics -that will affect virtually all stocks. No one can tell you when these traumas will occur -not me, not Charlie, not economists, not the media. [...] During such scary periods, you should never forget two things: First, widespread fear is your friend as an investor, because it serves up bargain purchases. Second, personal fear is your enemy. It will also be unwarranted. Investors who avoid high and unnecessary costs and simply sit for an extended period with a collection of large, conservatively-financed American businesses will almost certainly do well. “

Tags:

Reach out today. This could be the start of a great relationship.

Contact Us